Free Connecticut 8379 Form

Free Connecticut 8379 Form

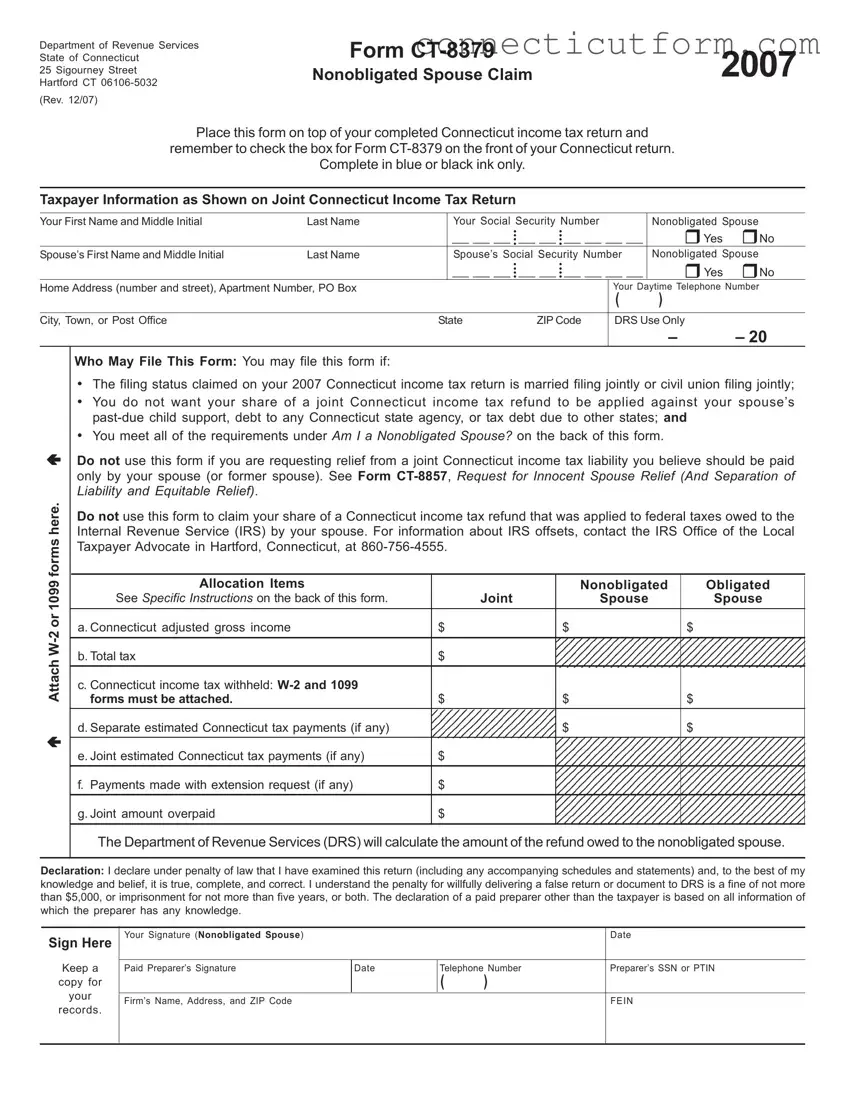

The Connecticut 8379 form serves as a critical resource for married or civil union partners who file their income tax returns jointly but do not want their share of the refund to be used for the spouse’s past-due debts, such as child support, debts to the state of Connecticut, or tax debts to other states. This form, formally titled the "Nonobligated Spouse Claim," requires detailed taxpayer information and demands precise documentation concerning income, tax withheld, and payments made, enabling the Department of Revenue Services (DR seniors) to accurately distinguish the nonobligated spouse’s tax obligations from those of their partner. The form outlines specific instructions on how to allocate income and payments between the spouses, providing a clear pathway for those who are not responsible for their spouse’s debts to claim their rightful share of the tax refund. Additionally, by including categories for allocation items and requiring declarations and signatures, the form ensures transparency and accountability in the filing process. The State of Connecticut has made provisions through Form CT-8379 for those seeking relief from their spouse’s financial liabilities, establishing a solid framework that recognizes the individual tax rights and responsibilities within a jointly filed return.

Department of Revenue Services

State of Connecticut

25 Sigourney Street

Hartford CT

(Rev. 12/07)

Form |

2007 |

Nonobligated Spouse Claim |

Place this form on top of your completed Connecticut income tax return and

remember to check the box for Form

Complete in blue or black ink only.

Taxpayer Information as Shown on Joint Connecticut Income Tax Return

Your First Name and Middle Initial |

Last Name |

|

Your Social Security Number |

|

Nonobligated Spouse |

|||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

Nonobligated Spouse |

|

Spouse’s First Name and Middle Initial |

Last Name |

|

Spouse’s Social Security Number |

|||||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

|

|

Home Address (number and street), Apartment Number, PO Box |

|

|

|

|

Your Daytime Telephone Number |

|||

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

City, Town, or Post Office |

|

State |

ZIP Code |

DRS Use Only |

|

|||

|

|

|

|

|

|

|

– |

– 20 |

Attach

Who May File This Form: You may file this form if:

•The filing status claimed on your 2007 Connecticut income tax return is married filing jointly or civil union filing jointly;

•You do not want your share of a joint Connecticut income tax refund to be applied against your spouse’s

•You meet all of the requirements under Am I a Nonobligated Spouse? on the back of this form.

Do not use this form if you are requesting relief from a joint Connecticut income tax liability you believe should be paid only by your spouse (or former spouse). See Form

Do not use this form to claim your share of a Connecticut income tax refund that was applied to federal taxes owed to the Internal Revenue Service (IRS) by your spouse. For information about IRS offsets, contact the IRS Office of the Local Taxpayer Advocate in Hartford, Connecticut, at

|

Allocation Items |

|

Nonobligated |

Obligated |

|

See Specific Instructions on the back of this form. |

Joint |

Spouse |

Spouse |

|

|

|

|

|

|

a. Connecticut adjusted gross income |

$ |

$ |

$ |

|

|

|

|

|

|

b. Total tax |

$ |

|

|

|

|

|

|

|

|

c. Connecticut income tax withheld: |

|

|

|

|

forms must be attached. |

$ |

$ |

$ |

|

|

|

|

|

|

d. Separate estimated Connecticut tax payments (if any) |

|

$ |

$ |

|

|

|

|

|

|

e. Joint estimated Connecticut tax payments (if any) |

$ |

|

|

|

|

|

|

|

|

f. Payments made with extension request (if any) |

$ |

|

|

|

|

|

|

|

|

g. Joint amount overpaid |

$ |

|

|

|

|

|

|

|

The Department of Revenue Services (DRS) will calculate the amount of the refund owed to the nonobligated spouse.

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to DRS is a fine of not more than $5,000, or imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Sign Here

Keep a

copy for

your

records.

Your Signature (Nonobligated Spouse) |

|

|

|

Date |

|

|

|

|

|

Paid Preparer’s Signature |

Date |

Telephone Number |

Preparer’s SSN or PTIN |

|

|

|

( |

) |

|

|

|

|

|

|

Firm’s Name, Address, and ZIP Code |

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

Form

Purpose: Use Form

•You are a nonobligated spouse and all or part of your overpayment was (or is expected to be) applied against:

•Your spouse’s past due State of Connecticut debt (such as child support, student loan, or any debt to any Connecticut state agency); or

•A tax debt due to other states; and

•You want your share of the joint overpayment refunded to you.

Any reference in this document to a spouse also refers to a party to a civil union recognized under Connecticut law.

General Instructions

Am I a Nonobligated Spouse?

You are a nonobligated spouse, if you meet all of the following requirements:

•You filed a joint Connecticut income tax return with a spouse who owes

•You received income (such as wages, interest, etc.) reported on the joint return;

•You made Connecticut income tax payments (such as withholding or estimated tax payments) reported on the joint return;

•You do not owe

•You filed a joint return reporting an overpayment of Connecticut income tax, all or part of which was or is expected to be applied against

Filing the Return: You must file Form

You must place this form on top of the completed Connecticut income tax return. If you previously filed your 2007 Connecticut income tax return, mail this form separately to: Department of Revenue Services, PO Box 5035, Hartford CT

Important: Attach copies of all forms

showing Connecticut income tax withheld to Form CT- 8379.

Specific Instructions

Taxpayer Information: Enter the taxpayer information exactly as it appears on your Connecticut income tax return. The name and Social Security Number (SSN) entered first on the joint tax return must also be entered first on Form

Allocation Items

a.Connecticut adjusted gross income: Enter the joint amount as reported on your joint Connecticut income tax return (Form

Nonresidents and

Nonresidents and |

Connecticut Source Income |

|

(Form |

||

Only |

||

|

Allocation Item

Joint

Nonobligated Spouse

Obligated Spouse

b.Total tax: Enter the joint Connecticut tax liability as reported on your joint Connecticut income tax return (Form

c.Connecticut income tax withheld: Enter the joint Connecticut withholding as reported on your joint Connecticut income tax return (Form

d.Separate estimated Connecticut tax payments: Enter any separately paid estimated Connecticut income tax payments in the appropriate spaces.

e.Joint estimated Connecticut tax payments: Enter the total amount of any joint estimated Connecticut income tax payments. Include overpayments applied from a previous year.

f.Payments made with extension request: Enter the joint amount as reported on your joint Connecticut income tax return (Form

g.Joint amount overpaid: Enter the joint amount overpaid as reported on your joint Connecticut income tax return (Form

Nonobligated Spouse Refund: DRS will calculate the amount of the nonobligated spouse’s refund. The nonobligated spouse’s share of the joint Connecticut tax overpayment cannot exceed the joint overpayment.

Signature: The nonobligated spouse must sign this form.

Others Who May Sign for the Nonobligated Spouse: Anyone with a signed Power of Attorney may sign on behalf of the nonobligated spouse. Attach a copy of the Power of Attorney.

Paid Preparer’s Signature: Anyone you pay to prepare your return must sign and date it. Paid preparers must also enter their SSN or Personal Tax Identification Number (PTIN), and their firm’s Federal Employer Identification Number (FEIN) in the spaces provided.

Form

| Fact | Details |

|---|---|

| Purpose | Form CT-8379, Nonobligated Spouse Claim, is used by individuals who do not want their share of a joint Connecticut income tax refund to be applied against their spouse’s past-due child support, state agency debt, or other states’ tax debts. |

| Eligibility | To be eligible, individuals must file jointly and meet certain conditions, such as not owing any past-due child support or agency debts themselves, and part of their joint tax refund is expected to be applied to the spouse's debts. |

| Required Attachments | All forms W-2 and 1099 showing Connecticut income tax withheld must be attached to Form CT-8379 for processing. |

| Governing Law | Form CT-8379 is governed by Connecticut state law, specifically addressing the tax filing and refund processes for married or civil union couples filing jointly in the state of Connecticut. |

Filing Form CT-8379 is crucial when you don't want your share of a Connecticut income tax refund to be used for your spouse's past debts, such as child support or state-owed obligations. Carefully completing this form ensures that your portion of any refund is protected. Below, find a step-by-step guide that will help you fill out the form accurately and efficiently.

Finishing this process correctly is paramount. Once completed, remember to place the form on top of your Connecticut income tax return, marking the appropriate box for Form CT-8379 on the front of your return. If your Connecticut income tax return was already filed, you'll need to send Form CT-8379 separately to the specified address. This detailed completion will ensure your rights are preserved and that only your spouse's share of the refund is available for debt offset.

Who should file Form CT-8379 in Connecticut?

If you're married or in a civil union and file jointly in Connecticut, but don't want your portion of a state income tax refund to be used for your spouse's debts like past-due child support, state agency debts, or tax debts to other states, Form CT-8379 is for you. It's not for those seeking relief from joint tax liabilities or whose refund was taken for federal IRS debts.

What requirements must I meet to be considered a nonobligated spouse?

To qualify, you must have filed a joint tax return where only your spouse has past-due debts as described, you must have reported income on this return, contributed to the tax payments, not owe any such debts yourself, and an overpayment was or is expected to be applied to these debts.

How do I file Form CT-8379?

Place Form CT-8379 on top of your Connecticut tax return when filing. If you already filed your return, you can send Form CT-8379 separately to the Department of Revenue Services. Ensure to check the box for Form CT-8379 on your tax return and attach any W-2 or 1099 forms showing Connecticut tax withheld.

What information do I need to provide on Form CT-8379?

Provide details as they appear on your joint income tax return, allocate your and your spouse's portions of income, tax liabilities, withholdings, estimated payments, and overpayments accordingly. Attach your W-2 or 1099 forms as well.

How is the refund calculated for a nonobligated spouse?

The Connecticut Department of Revenue Services will calculate your refund based on the portion of the overpayment that is attributable to you, not exceeding the total joint overpayment amount.

What happens if I filled out the form incorrectly?

If errors are found, it could delay processing. Ensure all information matches what was submitted on your joint tax return and verify that your calculations are correct.

Can I file Form CT-8379 electronically?

As of the last update, you must submit this form in paper form along with your tax return. If filed after the fact, mail it directly to the specified address of the Department of Revenue Services.

What should I do if I don't agree with the debt claimed by my spouse?

Form CT-8379 isn't for disputing the validity of the debt. If you disagree with the debt itself, contact the agency to which the debt is owed. For disagreements on the tax burden allocation, consider Form CT-8857 for Innocent Spouse Relief.

Who can sign Form CT-8379 on behalf of the nonobligated spouse?

The nonobligated spouse must sign the form. If they are unable to, a representative holding Power of Attorney may sign, but a copy of the Power of Attorney must be attached. Paid preparers must also sign, date, and provide their identification numbers.

Filling out the Connecticut Form CT-8379, the Nonobligated Spouse Claim, can be a tricky process filled with potential pitfalls. Designed for spouses seeking their share of a joint tax refund that might otherwise be applied to the other spouse's debts, such as back taxes, child support, or state agency debts, it's essential to get it right. Here are seven common mistakes people make:

Avoiding these mistakes is key to ensuring that the process of claiming a rightful share of a joint tax refund goes smoothly. It's not just about filling in the blanks; it's about paying close attention to detail, understanding each section, and providing accurate and complete information. This helps ensure that the Department of Revenue Services can process the form efficiently, leading to a quicker resolution and refund payment. Whether you're dealing with withheld wages, student loan debts, or other financial binds connected to your spouse, Form CT-8379 is a critical tool in preserving your financial rights.

In conclusion, properly completing Form CT-8379 demands thoroughness, accuracy, and an understanding of its requirements. By avoiding these common mistakes, filers can better navigate the complexities of tax filings, ensuring that both parties' financial interests are properly represented and protected.

When navigating the complexities of tax claims in Connecticut, especially involving situations like the nonobligated spouse claim, a variety of forms and documents alongside Form CT-8379 can play crucial roles. Understanding these additional forms helps ensure taxpayers are well-prepared and can secure their rightful claims effectively.

Together, these forms and documents encompass the breadth of resources available to taxpayers in Connecticut, particularly when dealing with the allocation of tax liabilities and refunds between spouses. Accurate and informed use of each can greatly impact the efficiency and success of navigating tax obligations and protecting individual rights within the tax system.

The Connecticut 8379 form is similar to other forms designed to offer relief or assert rights under specific tax filing statuses. These documents help taxpayers navigate their obligations in scenarios that require a detailed declaration of individual finances and liabilities, often involving joint filings with a spouse. Each form, while unique in its purpose and application, shares commonalities with the Connecticut 8379 form in terms of providing protections or remediation for taxpayers under specific circumstances.

One such document is the IRS Form 8379, Injured Spouse Allocation. This form serves a similar purpose at the federal level to what Connecticut’s Form 8379 accomplishes at the state level. It is designed for taxpayers who do not wish for their portion of a joint tax refund to be applied to their spouse’s past due federal debts, such as federal taxes, child or spousal support, and federal non-tax debts, like student loans. Both forms require details on income, tax payments, and withheld amounts, allocated between the spouses, to properly calculate the non-obligated party’s share of the overpayment. They also share a fundamental goal: to protect the financial interests of a spouse who is not responsible for the other’s debts.

Another related document is Form CT-8857, Request for Innocent Spouse Relief (And Separation of Liability and Equitable Relief). Though it serves a markedly different function, it bears relevance through its connection to tax liabilities arising from joint filings. While the CT-8379 form focuses on refund allocations and not applying one spouse's refund to cover the debts of the other, Form CT-8857 allows a taxpayer to apply for relief from joint tax liabilities if it would be unfair to hold them responsible for the understatement or understatement of tax due to actions of their spouse or ex-spouse. This includes scenarios where one spouse may have erroneously reported income or claimed deductions. The underlying similarity is the recognition of individual rights within the joint filing context, and the legal mechanisms to protect those rights.

Each document underscores the complexities of tax law and the recognition of individual circumstances within the framework of joint financial responsibilities. They highlight the mechanisms available to taxpayers seeking to ensure fair treatment under the law, reflecting a nuanced understanding of personal and shared financial obligations.

When you're filling out the Connecticut 8379 form, there are specific dos and don'ts that can help ensure your form is processed smoothly and correctly. Below are important points to consider.

Things You Should DoUnderstanding taxation and its related forms can be a real maze, especially when it comes to specific situations like filing Form CT-8379 in Connecticut. It's designed for a unique scenario - when one spouse does not want their joint tax refund applied to the other spouse's outstanding debts. Let's unravel some common misconceptions about this form to ensure you have all the facts straight.

Misconception 1: Form CT-8379 is for filing separate taxes. In reality, this form is specifically for married couples or those in a civil union who file jointly but want to protect one spouse's portion of a tax refund from being applied to the other's debts, such as past-due child support, state agency debts, or debts to other states.

Misconception 2: Any couple can file Form CT-8379. Only couples who filed jointly and where one spouse is not responsible for the other's specific debts can use this form. It's not a one-size-fits-all solution and requires meeting specific eligibility criteria.

Misconception 3: You can use Form CT-8379 to separate liabilities on other taxes. This form only applies to the Connecticut income tax overpayment and its potential refund. It doesn't separate liabilities for other taxes or ensure that future refunds are divided.

Misconception 4: Filing Form CT-8379 will delay your refund. While it's true that additional documentation and review might take time, the form itself is designed to ensure that the nonobligated spouse gets their fair share of the refund without undue delay attributable to the form's processing.

Misconception 5: Form CT-8379 is only for protecting refunds from child support claims. Although child support is a common debt that can claim a tax refund, this form also applies to debts owed to any Connecticut state agency or tax debts to other states.

Misconception 6: You don't need to attach income documentation. On the contrary, attaching forms W-2 and 1099 showing Connecticut income tax withheld is crucial for filing Form CT-8379. This documentation is necessary to calculate the nonobligated spouse's share of the refund accurately.

Misconception 7: The form can be used for federal tax issues. Form CT-8379 only deals with Connecticut state tax refunds. For federal tax issues or to protect a federal refund from being offset for a spouse's debts, other forms and procedures with the IRS are involved.

Misconception 8: The nonobligated spouse doesn't need to sign Form CT-8379. In fact, the form requires the signature of the nonobligated spouse to be valid. If the nonobligated spouse cannot sign, a Power of Attorney may do so, but proper documentation must be attached.

Misconception 9: Once you file Form CT-8379, you don't have to file it again for future tax years. Each tax year is separate, and if the same conditions apply, the form needs to be filed each year with the joint tax return to protect the nonobligated spouse's refund.

Understanding these points can clear up confusion and help ensure that couples in Connecticut navigate their tax responsibilities effectively, especially when it comes to managing individual liabilities and entitlements in a joint tax refund scenario.

Understanding the Connecticut Form CT-8379 for Nonobligated Spouses is crucial for couples dealing with specific financial disputes. Here are seven key takeaways to guide individuals through this process:

By adhering to these guidelines, nonobligated spouses can navigate the complexities of safeguarding their portion of a joint tax refund in Connecticut.

Sample Accident Report Form - A checklist for the reporting officer to confirm the accuracy and completion of the report helps maintain the reliability of the information.

Connecticut Withholding Employer Login - Businesses can seek assistance from the Connecticut Department of Labor for guidance on filling out and submitting the UC-2 Form correctly.

Connecticut Eviction Notice Download - Clarification on achieving Default Judgments in eviction cases, outlining scenarios where tenants fail to respond or appear in court.