Free Connecticut Au 738 Form

Free Connecticut Au 738 Form

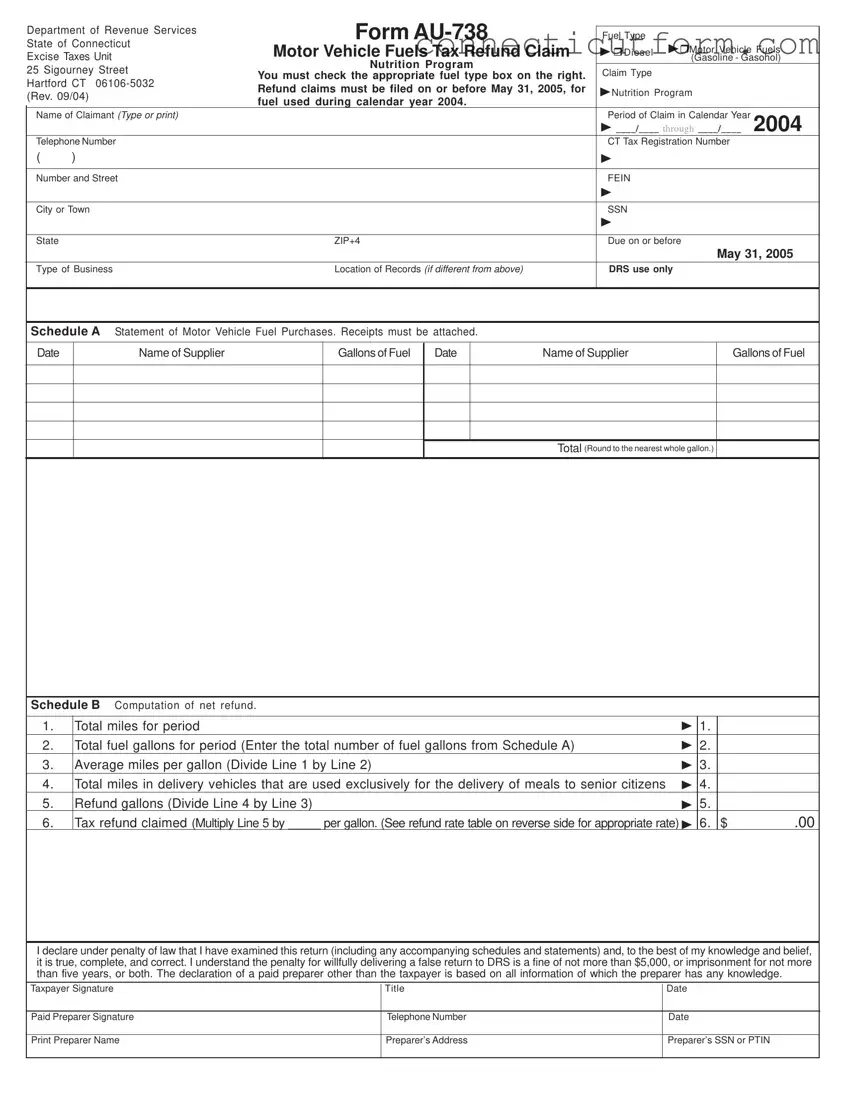

The Connecticut Au 738 form is a crucial document for those seeking a motor vehicle fuels tax refund from the Department of Revenue Services. Specifically designed for fuel types like diesel, gasoline, and gasohol, this form facilitates the refund claim process for excise taxes under the State of Connecticut's Motor Vehicle Fuels Tax Refund Claim umbrella. Located at 25 Sigourney Street, Hartford CT 06106-5032, the Excise Taxes Unit requires this form to be filed no later than May 31, 2005, for fuel utilized during the 2004 calendar year. Crucial to those in the nutrition program, claimants must meticulously indicate their fuel type, alongside personal and business information, ensuring eligibility for the refund. This process involves submitting detailed records of motor vehicle fuel purchases, including receipts, and calculating the net refund based on specific criteria related to the delivery of meals to senior citizens. The form underscores the importance of accuracy and compliance, warning of severe penalties for false returns. With its comprehensive instructions and requirement for detailed documentation, Form AU-738 serves as a vital tool for eligible businesses or individuals in Connecticut to recoup a portion of the fuel taxes paid, enabling them to better support vital services such as the delivery of meals to senior citizens.

Department of Revenue Services |

|

Form |

|

Fuel Type |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||

State of Connecticut |

Motor Vehicle Fuels Tax Refund Claim |

Diesel |

(Gasoline - Gasohol) |

|||||||||

Excise Taxes Unit |

||||||||||||

|

|

|

|

|

|

|

|

|

Motor Vehicle Fuels |

|||

25 Sigourney Street |

|

Nutrition Program |

|

|

|

|

|

|

||||

|

|

Claim Type |

|

|

|

|

||||||

You must check the appropriate fuel type box on the right. |

|

|

|

|

||||||||

Hartford CT |

|

|

|

|

||||||||

Refund claims must be filed on or before May 31, 2005, for |

Nutrition Program |

|

||||||||||

(Rev. 09/04) |

|

|||||||||||

fuel used during calendar year 2004. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

||||

Name of Claimant (Type or print) |

|

|

|

|

|

Period of Claim in Calendar Year |

2004 |

|||||

|

|

|

|

|

|

|

|

____/____ through ____/____ |

||||

Telephone Number |

|

|

|

|

|

CT Tax Registration Number |

|

|||||

( |

) |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Number and Street |

|

|

|

|

|

FEIN |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or Town |

|

|

|

|

|

SSN |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

|

|

ZIP+4 |

|

|

|

Due on or before |

|

|||

|

|

|

|

|

|

|

|

|

|

|

May 31, 2005 |

|

Type of Business |

|

Location of Records (if different from above) |

|

DRS use only |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

Schedule A Statement of Motor Vehicle Fuel Purchases. Receipts must be attached. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Date |

|

Name of Supplier |

|

Gallons of Fuel |

Date |

|

Name of Supplier |

|

|

Gallons of Fuel |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total (Round to the nearest whole gallon.) |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule B Computation of net refund. |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

1. |

Total miles for period |

|

|

|

|

|

|

1. |

|

|

||

2. |

Total fuel gallons for period (Enter the total number of fuel gallons from Schedule A) |

|

2. |

|

|

|||||||

3. |

Average miles per gallon (Divide Line 1 by Line 2) |

|

|

|

|

3. |

|

|

||||

4. |

Total miles in delivery vehicles that are used exclusively for the delivery of meals to senior citizens |

4. |

|

|

||||||||

5. |

Refund gallons (Divide Line 4 by Line 3) |

|

|

|

|

5. |

|

|

||||

6. |

|

Tax refund claimed (Multiply Line 5 by _____ per gallon. (See refund rate table on reverse side for appropriate rate) |

6. |

$ |

.00 |

|||||||

I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return to DRS is a fine of not more than $5,000, or imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Taxpayer Signature |

Title |

Date |

|

|

|

Paid Preparer Signature |

Telephone Number |

Date |

|

|

|

Print Preparer Name |

Preparer’s Address |

Preparer’s SSN or PTIN |

|

|

|

Instructions

Your motor vehicle fuels tax refund claim for fuel used during calendar year 2004 must:

1.Be filed with Department of Revenue Services (DRS) on or before May 31, 2005; and

2.Involve at least 200 gallons of fuel eligible for tax refund.

The appropriate fuel type box must be marked on the front of this form in order to process this claim. You must file a separate Form

Be sure to provide a telephone number where you can be contacted.

You must indicate your Connecticut tax registration number or Social Security Number in the space provided.

For all purchases of fuel listed, you must attach a copy of each numbered slip or invoice issued at the time of the purchase. The slip or invoice may be the original or a photocopy and must show the:

•Date of purchase;

•Name and address of the seller (which must be printed or rubber stamped on the slip or invoice);

•Name and address of the purchaser (which must be the name and address of the person or entity filing the claim for refund);

•Number of gallons of fuel purchased;

•Price per gallon;

•Total amount paid; and

•If payment is made within a discounted period, provide proof of amount paid.

You must retain records to substantiate your refund claim for at least three years following the filing of the claim and make them

Table of Motor Vehicle Fuels Tax Refund Rates for 2004

for Nutrition Program

Diesel January 1, 2004 |

through |

December 31, 2004 |

26¢ |

per Gallon |

Motor Vehicle Fuels |

|

|

|

|

January 1, 2004 |

through |

December 31, 2004 |

25¢ |

per Gallon |

Note: You must file a separate Form

available to DRS upon request.

Rounding Off to Whole Dollars: You must round off cents to the nearest whole dollar on your motor vehicle fuels tax refund claim. Round down to the next lowest dollar all amounts that include 1 through 49 cents. Round up to the next highest dollar all amounts that include 50 through 99 cents. However, if you need to add two or more amounts to compute the total to enter on a line, include cents and round off only the total.

Example: Add two amounts ($1.29 + $3.21) to compute the total ($4.50) to enter on a line. $4.50 is rounded to $5.00 and entered on the line.

You must attach a copy of your contract with your local area agency on aging as evidence of your eligibility to provide Title

Mail the completed refund application to: Department of Revenue Services State of Connecticut

Excise Taxes Unit

25 Sigourney Street Hartford CT

Additional Information

If you need additional information or assistance, please call the Excise Taxes Unit at

www.ct.gov/DRS

Your refund will be applied against any outstanding DRS tax liability.

Form

| Fact | Detail |

|---|---|

| Form Purpose | To claim a refund for motor vehicle fuels tax for fuel used in the delivery of meals to senior citizens. |

| Eligibility Criteria | Must have used the fuel during the calendar year 2004 for nutrition programs, specifically for the delivery of meals to senior citizens. |

| Deadlines | Refund claims must be submitted on or before May 31, 2005. |

| Governing Law | Administered by the Connecticut Department of Revenue Services under the state's excise tax laws related to motor vehicle fuels. |

Filing out the Connecticut AU-738 form is a systematic process that, when followed precisely, ensures adherence to the guidelines set by the Department of Revenue Services. This documentation is crucial for entities claiming a motor vehicle fuels tax refund, specifically pertaining to fuel utilized within a calendar year. Offering a clear path to reclaim taxes requires an accurate, detailed completion of this form. Below is a guide to assist in this process:

Once submitted, the Department of Revenue Services will process the refund claim. It is crucial that all documentation is retained for at least three years following the claim to support the refund request if needed. This careful preparation aids in a smooth claims process, potentially offsetting any outstanding tax liabilities with the Department of Revenue Services. Should further assistance be necessary, the Excise Taxes Unit is available to provide support.

What is the purpose of the Connecticut AU-738 form?

The Connecticut AU-738 form is specifically designed for individuals or entities to claim a tax refund on motor vehicle fuels, such as diesel, gasoline, and gasohol. This form facilitates the process for claimants who have used fuel for purposes that qualify for a tax refund, notably for vehicles used exclusively in the delivery of meals to senior citizens as part of a Nutrition Program.

Who needs to file the AU-738 form?

Any individual or entity that has purchased motor vehicle fuels within the state of Connecticut and has used these fuels for purposes that are eligible for a tax refund must file the Form AU-738. This is particularly aimed at those involved in the delivery of meals to senior citizens under the Nutrition Program.

By when must the Form AU-738 be filed?

Claims for the tax refund on motor vehicle fuels used within a calendar year must be filed with the Department of Revenue Services (DRS) by May 31 of the following year. For example, for fuel used during the calendar year 2004, the claim must be filed on or before May 31, 2005.

What documentation is required to file this form?

How is the refund calculated?

The refund is calculated based on the total miles driven by delivery vehicles exclusively used for the purpose mentioned (delivering meals to senior citizens), the total gallons of fuel purchased, and the average miles per gallon. The calculation involves determining the gallons of fuel used exclusively for eligible delivery activities and applying the specific tax refund rate per gallon.

What are the important deadlines and requirements to remember when filing this form?

Key requirements include filing the claim by the May 31 deadline following the year of fuel usage, ensuring that at least 200 gallons of fuel were purchased for eligible purposes, and rounding off cents to the nearest whole dollar on the refund claim. Additionally, retaining records to substantiate the refund claim for at least three years after filing is crucial for verification purposes by DRS.

Where can additional information or assistance be found?

For further information or help with the AU-738 form, the Excise Taxes Unit of the Department of Revenue Services can be contacted at 860-541-3224, Monday through Friday, 8:00 a.m. to 5:00 p.m. Forms and additional guidance can also be downloaded from the DRS website at www.ct.gov/DRS.

Filling out the Connecticut AU-738 form can be a complicated process, and errors can delay or even negate your refund claim. Understanding the common mistakes made by applicants can help ensure your submission is processed quickly and accurately.

One common error involves the fuel type selection. Applicants must check the appropriate fuel type box on the right side of the form. This may seem trivial, but selecting the wrong fuel type can lead to the rejection of your claim. The form differentiates between diesel, gasoline, and gasohol, each having distinct tax refund rates and requirements.

Another frequent mistake is the failure to attach required documentation. For the refund to be processed, copies of numbered slips or invoices for all fuel purchases listed in Schedule A must be included with the form. These documents must show detailed information, including the date of purchase, amount of fuel bought, and the total paid. Additionally, evidence of your contract with your local area agency on aging must be attached to verify your eligibility to provide Title III-C meals to seniors.

Avoiding these mistakes requires careful reading of the form instructions and thorough preparation of your claim. It’s also advisable to retain copies of your submission and all supporting documents for at least three years, as you may need to present these records upon request by the Department of Revenue Services.

In summary, when filling out the Connecticut AU-738 form, ensure to select the correct fuel type, attach all necessary documentation, accurately compute your refund amount, and adhere to the submission deadline. By avoiding these common errors, you can streamline the process of claiming your motor vehicle fuels tax refund.

When filing Form AU-738 in Connecticut, a document aiming to claim motor vehicle fuels tax refunds, particularly for delivering meals to senior citizens and similar nutrition programs, certain supportive documentation often supplements it. This approach ensures compliance with taxation laws while maximizing an entity's ability to achieve rightful refunds. These documents not only provide a basis for the claimed refund but also aid in establishing a transparent and verifiable trail of fuel usage and entitlement under specific tax laws.

Together, these documents form a robust packet accompanying the Connecticut AU-738 form, grounding the fuel tax refund claim in well-documented evidence. This comprehensive approach safeguards both the claimant's interests and the tax authorities' need for due diligence, ensuring a smooth, transparent, and efficient refund process for eligible fuel used in service to community nutrition programs.

The Connecticut AU-738 form, utilized for motor vehicle fuels tax refund claims, shares similarities with various tax-related documents concerning its structure and the type of information it requires from the applicant. One such document is the Federal Form 4136, also known as the "Credit for Federal Tax Paid on Fuels" form.

Federal Form 4136 serves a purpose akin to the Connecticut AU-738 form in that it allows taxpayers to claim credits or refunds for certain types of fuel taxes. Both documents require the claimant to report detailed information regarding fuel purchases, including the type of fuel, total gallons purchased, and the tax rate applicable to those purchases. Additionally, they necessitate submissions of supporting documentation, such as purchase receipts or invoices, to substantiate the claim. The key difference lies in their jurisdictional application; Form 4136 applies to federal taxes, whereas the AU-738 form is specific to the state of Connecticut.

Another document resembling the AU-738 form is the IRS Form 8849, the "Claim for Refund of Excise Taxes". This form also involves claiming refunds for overpaid taxes on fuels among various other excise taxes. Similar to the AU-738, Form 8849 requires detailed listings of purchases, including the amount of fuel and the taxes paid. However, Form 8849 covers a broader range of tax refund claims beyond just fuel, including communications and air transportation taxes, making it applicable for a wider range of taxpayers seeking refunds for different types of excise taxes. The alignment between these forms is primarily found in their structured approach to documenting tax claims related to fuel usage, albeit for different jurisdictions and types of excise taxes.

The common thread among these documents is their role in offering taxpayers a means to claim refunds on taxes paid on fuel, underlining the importance of accurate record-keeping and adherence to specific filing deadlines. Each form, whether for state-level or federal refunds, demands a thorough compilation of fuel purchase information, proof of payment, and a clear calculation of the refund amount based on precise tax rates. The specific requirements and the context of use might differ, but they all share the goal of ensuring taxpayers can reclaim amounts owed to them due to overpayment or specific tax relief programs.

Filling out the Connecticut AU-738 form correctly is crucial for submitting a successful Motor Vehicle Fuels Tax Refund Claim. Below are guidelines to ensure your submission is accurate and compliant with the Department of Revenue Services requirements.

Do's:

Don'ts:

There are several misconceptions about the Connecticut AU-738 form, a document integral to claiming motor vehicle fuels tax refunds. Understanding these misconceptions can provide clarity and improve the process of filing a claim.

In conclusion, understanding these aspects of the AU-738 form can help applicants accurately claim their rightful motor vehicle fuels tax refund, avoiding common pitfalls and errors that could delay or invalidate their claim.

Filling out and using the Connecticut AU-738 form for claiming a motor vehicle fuels tax refund requires close attention to detail and an understanding of the eligibility requirements. Here are key takeaways to ensure a smooth and successful submission process:

Mail your completed application to the specified address of the Department of Revenue Services' Excise Taxes Unit in Hartford, CT. Always remember, proper documentation and adherence to guidelines enhance the likelihood of a successful tax refund claim.

For any additional information or assistance, contact the Excise Taxes Unit during their business hours. Forms and further instructions can also be downloaded from the Connecticut Department of Revenue Services website.

Change of Address Form Ct - This document allows for simultaneous updates to one's driving license, non-driver ID, and vehicle registrations, including vessels, upon a change of address.

Injured Spouse Claim - Form CT-8379 stands as a beacon of financial fairness, enabling spouses to assert their rightful claim to tax refunds without the shadow of joint liabilities.

Connecticut Unemployment Employer Login - The location, Houston, relates the form to a specific geographic area, aiding in localized public health monitoring and intervention strategies.