Free Connecticut Op 300 Form

Free Connecticut Op 300 Form

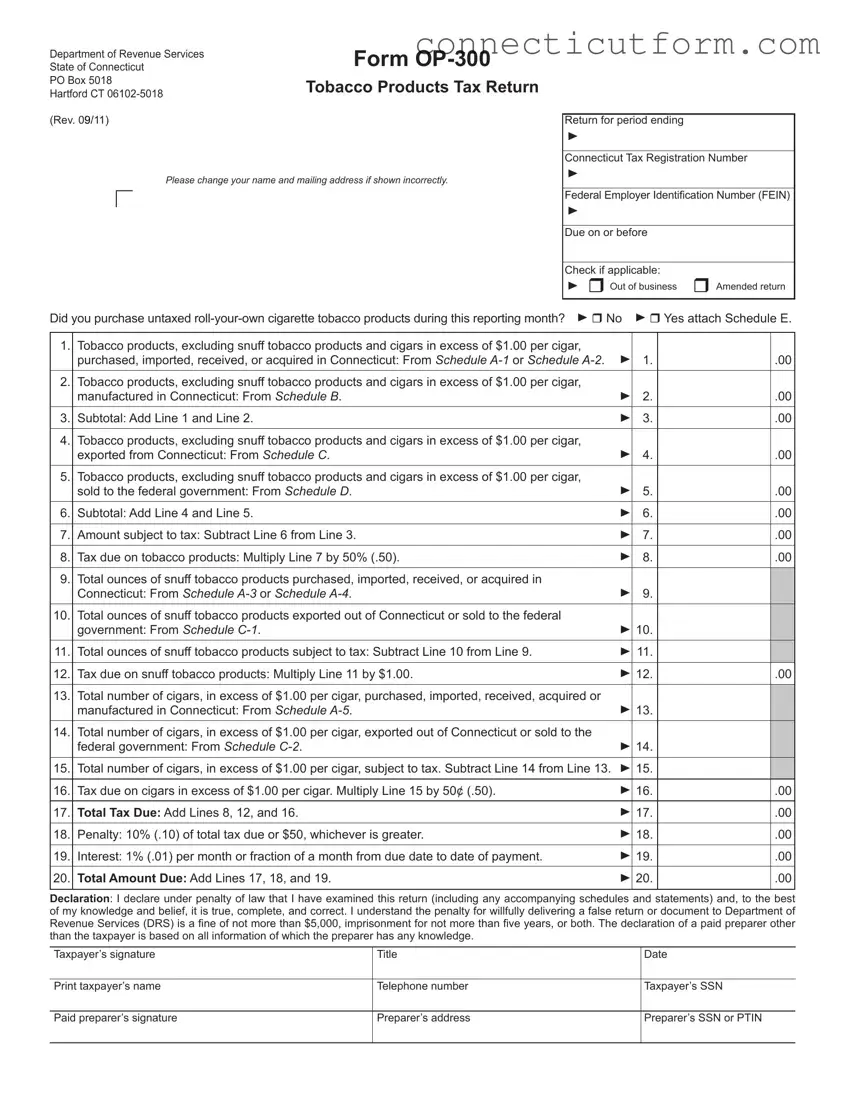

Every business dealing with tobacco products in the state of Connecticut must navigate the complexities of tax obligations, and the Connecticut OP-300 form serves as a crucial tool in this process. Essentially, this document, issued by the Department of Revenue Services, is designed for the detailed reporting of tobacco products taxes. Businesses are required to meticulously report various categories of tobacco products, including but not limited to snuff, cigars priced over $1.00, and other smoking or chewing tobacco products that have been purchased, imported, acquired, or manufactured within Connecticut. The form also addresses exports and sales to the federal government, distinguishing between different types of tobacco products for tax purposes. Calculating the taxes due involves several steps; initially, businesses must determine the total amount of each product category they handle. Subsequently, they apply specific tax rates—50% of the value for certain tobacco products and $1.00 per ounce for snuff, with a distinct procedure for cigars exceeding$1.00 each. Critical to this process is the adherence to deadlines, as the form must be filed monthly by the 25th day following the reporting month. Penalties for late submissions are clearly outlined, underscoring the importance of timely compliance. Additionally, the form provides a section for declaring amendments or business status changes, such as closure. For ease of use and ensuring accuracy, electronic payment options are highly encouraged, highlighting the state's push towards streamlined, efficient tax reporting and payment systems. This brief overview underscores the form's integral role in the regulatory landscape, guiding businesses through their fiscal duties while also contributing to the state's financial health.

Department of Revenue Services |

Form |

|

State of Connecticut |

||

PO Box 5018 |

Tobacco Products Tax Return |

|

Hartford CT |

||

|

||

(Rev. 09/11) |

|

Please change your name and mailing address if shown incorrectly.

Return for period ending

Connecticut Tax Registration Number

Federal Employer Identiication Number (FEIN)

Due on or before

Check if applicable:

Out of business Amended return

Did you purchase untaxed

1. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

purchased, imported, received, or acquired in Connecticut: From Schedule |

|

1. |

|

.00 |

|

|

|

|

|

|

2. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

manufactured in Connecticut: From Schedule B. |

|

2. |

|

.00 |

|

|

|

|

|

|

3. |

Subtotal: Add Line 1 and Line 2. |

|

3. |

|

.00 |

|

|

|

|

|

|

4. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

exported from Connecticut: From Schedule C. |

|

4. |

|

.00 |

|

|

|

|

|

|

5. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

sold to the federal government: From Schedule D. |

|

5. |

|

.00 |

|

|

|

|

|

|

6. |

Subtotal: Add Line 4 and Line 5. |

|

6. |

|

.00 |

|

|

|

|

|

|

7. |

Amount subject to tax: Subtract Line 6 from Line 3. |

|

7. |

|

.00 |

|

|

|

|

|

|

8. |

Tax due on tobacco products: Multiply Line 7 by 50% (.50). |

|

8. |

|

.00 |

|

|

|

|

|

|

9. |

Total ounces of snuff tobacco products purchased, imported, received, or acquired in |

|

|

|

|

|

Connecticut: From Schedule |

|

9. |

|

|

10. |

Total ounces of snuff tobacco products exported out of Connecticut or sold to the federal |

|

|

|

|

|

government: From Schedule |

|

10. |

|

|

11. |

Total ounces of snuff tobacco products subject to tax: Subtract Line 10 from Line 9. |

|

11. |

|

|

12. |

Tax due on snuff tobacco products: Multiply Line 11 by $1.00. |

|

12. |

|

.00 |

|

|

|

|

|

|

13. |

Total number of cigars, in excess of $1.00 per cigar, purchased, imported, received, acquired or |

|

|

|

|

|

manufactured in Connecticut: From Schedule |

|

13. |

|

|

14. |

Total number of cigars, in excess of $1.00 per cigar, exported out of Connecticut or sold to the |

|

|

|

|

|

federal government: From Schedule |

|

14. |

|

|

15. |

Total number of cigars, in excess of $1.00 per cigar, subject to tax. Subtract Line 14 from Line 13. |

|

15. |

|

|

16. |

Tax due on cigars in excess of $1.00 per cigar. Multiply Line 15 by 50¢ (.50). |

|

16. |

|

.00 |

17. |

Total Tax Due: Add Lines 8, 12, and 16. |

|

17. |

|

.00 |

|

|

|

|

|

|

18. |

Penalty: 10% (.10) of total tax due or $50, whichever is greater. |

|

18. |

|

.00 |

|

|

|

|

|

|

19. |

Interest: 1% (.01) per month or fraction of a month from due date to date of payment. |

|

19. |

|

.00 |

|

|

|

|

|

|

20. |

Total Amount Due: Add Lines 17, 18, and 19. |

|

20. |

|

.00 |

|

|

|

|

|

|

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to Department of

Revenue Services (DRS) is a ine of not more than $5,000, imprisonment for not more than ive years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Taxpayer’s signature |

Title |

Date |

Print taxpayer’s name

Telephone number

Taxpayer’s SSN

Paid preparer’s signature

Preparer’s address

Preparer’s SSN or PTIN

General Instructions

Complete the return in blue or black ink only.

Taxpayers must ile a return for each calendar month by the

Example: The tobacco products tax return for January 1 through

January 31 must be iled on or before February 25.

Taxpayers must ile a return even if no tax is due. All

supporting schedules can be found on the Department of Revenue Services (DRS) website at www.ct.gov/DRS

The owner, a partner, or a principal oficer must sign this

return.

Pay Electronically: Visit www.ct.gov/TSC to use the Taxpayer Service Center (TSC) to make a direct tax

payment. After logging onto the TSC, select the Make Payment Only option and choose a tax type from the drop down box. Using this option authorizes the DRS to electronically withdraw from your bank account (checking or savings) a payment on a date you select up to the due date.

As a reminder, even if you pay electronically you must still ile your return by the due date. Tax not paid on or before the

due date will be subject to penalty and interest.

If you do not pay electronically, make check payable to Commissioner of Revenue Services. DRS may submit

your check to your bank electronically.

Mail to: Department of Revenue Services

State of Connecticut

PO Box 5018

Hartford CT

Deinitions

TOBACCO PRODUCTS means: Cigars, cheroots, stogies, periques, granulated, plug cut, crimp cut, ready rubbed and

other smoking tobacco, cavendish, plug and twist tobacco, ine cut and other chewing tobaccos, shorts, refuse scraps,

clippings, cuttings and sweepings of tobacco, and all other kinds and forms of tobacco prepared in a manner as to be suitable for chewing or smoking in a pipe or otherwise for both

chewing and smoking, but does not include any cigarettes as deined in Conn. Gen. Stat.

SNUFF TOBACCO PRODUCTS means: Tobacco products that have imprinted on the packages the designation “snuff” or

“snuff lour” or the federal tax designation “Tax Class M,” or

both.

WHOLESALE SALES PRICE means:

•In the case of a distributor that is the manufacturer of the tobacco products, the price set for these products or, if no price has been set, the wholesale value of these products.

•In the case of a distributor that is not the manufacturer of the tobacco products, the price at which the distributor purchased the products.

Speciic Instructions

Check Box: You must check the appropriate box concerning the purchase of untaxed

Line 1

Resident Distributor: Enter from Schedule

wholesale sales price of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar)

purchased, imported, received, or acquired in Connecticut by the distributor.

Nonresident Distributor: Enter from Schedule

tobacco products and cigars in excess of $1.00 per cigar)

imported into Connecticut by the distributor.

Line 2 - Enter from Schedule B the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) manufactured in

Connecticut by the distributor.

Line 4 - Enter from Schedule C the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) exported from Connecticut

that were imported, received, purchased, acquired, or manufactured in Connecticut by the distributor. Prepare a separate Schedule C for each state of destination. (Use Line 9 and Line 10 to report snuff products and Line 13 and

Line 14 to report cigars in excess of $1.00 per cigar.)

Line 5 - Enter from Schedule D the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) sold to the federal

government that were imported, received, purchased, acquired, or manufactured in Connecticut by the distributor.

Line 9 - Enter from Schedule

Line 10 - Enter from Schedule

Line 13 - Enter from Schedule

acquired, or manufactured in Connecticut.

Line 14 - Enter from Schedule

sold to the federal government.

For Further Information

If you need additional information or assistance, please call the Excise Taxes Unit at

Forms and Publications: Visit the DRS website at www.ct.gov/DRS to download and print Connecticut tax

forms and publications.

TTY, TDD, and Text Telephone users only may transmit inquiries anytime by calling

| Fact | Detail |

|---|---|

| Form Name | OP-300 Tobacco Products Tax Return |

| Revision Date | September 2011 |

| Administering Agency | Department of Revenue Services, State of Connecticut |

| Purpose | To report and pay tax on tobacco products excluding cigarettes |

| Due Date | Due on or before the twenty-fifth day of the month following the reporting period |

| Governing Law | Connecticut General Statutes, specifically referenced in Conn. Gen. Stat. §12-285 for definitions of tobacco products |

| Penalty for Late Filing | 10% of total tax due or $50, whichever is greater, plus 1% interest per month on overdue payment |

| Electronic Filing Option | Available through the Taxpayer Service Center (TSC) at www.ct.gov/TSC |

| Who Must File | Distributors of tobacco products in Connecticut, including both resident and non-resident distributors |

| Tax Rates | 50% (.50) of the value on certain tobacco products, $1.00 per ounce on snuff tobacco products, and 50¢ (.50) per cigar for cigars in excess of $1.00 |

| Supporting Schedules | Schedule E and others for detailed reporting of different categories of tobacco products |

Filling out the Connecticut OP-300 form is a straightforward process when you know what to expect and prepare the necessary information ahead of time. This form is essential for individuals or businesses that deal with tobacco products in Connecticut, ensuring compliance with state tax regulations. By following the steps below, taxpayers can accurately report and pay taxes on tobacco products, thus contributing to state revenue used for public services.

For further assistance, taxpayers can contact the Excise Taxes Unit or visit the DRS website for additional resources, including forms and instructions. Paying attention to deadlines, accurately reporting transactions, and promptly addressing any errors can prevent penalties and ensure compliance with Connecticut tobacco tax laws.

The Connecticut OP-300 Form, issued by the Department of Revenue Services, is a Tobacco Products Tax Return form. It records the activities related to the purchase, importation, manufacture, and sale of tobacco products within Connecticut, excluding cigarettes. It's for documenting taxes due on these transactions.

For each calendar month, the form must be filled out and submitted by the 25th day of the following month. For instance, the return covering January's activities is due by February 25th.

Any distributor of tobacco products (excluding cigarettes) in Connecticut, including both resident and non-resident distributors, is required to file the OP-300 form. This includes those who manufacture tobacco products within the state.

If you bought untaxed roll-your-own cigarette tobacco products during the reporting month, you must indicate this by checking the appropriate box on the form and attaching Schedule E.

Tax on tobacco products, other than snuff and cigars costing more than $1.00 per cigar, is calculated based on the wholesale sales price. The tax due is 50% (Line 8 on the form) of the amount subject to tax (Line 7). For snuff tobacco products, tax is calculated at $1.00 per ounce of total ounces subject to tax (Line 11). For cigars costing more than $1.00 each, the tax due is 50¢ per cigar on the total number subject to tax (Line 15).

Even if no tax is due, you are still required to file the OP-300 form for that month, indicating all zeros where applicable to show that there was no taxable activity.

Yes, payments can be made electronically through the Connecticut Department of Revenue Services website by selecting the Make Payment Only option. This authorizes the DRS to withdraw the payment directly from your bank account before the due date. Electronic filing of the return is also required even if you pay electronically.

If the tax is not paid or the return not filed by the due date, penalties and interest will be applied. The penalty is 10% of the total tax due or $50, whichever is greater (Line 18), and interest is calculated at 1% per month or fraction thereof from the due date until the payment is made (Line 19).

You can call the Excise Taxes Unit at 860-541-3224, Monday through Friday, from 8:30 a.m. to 4:30 p.m. for help. Also, the Department of Revenue Services website offers forms, publications, and further guidance.

Filling out the Connecticut OP-300 form, which pertains to the Tobacco Products Tax Return, is a task that demands attention to detail and a comprehensive understanding of the taxation requirements for tobacco products within the state. However, several common mistakes can hinder the accuracy and compliance of these submissions, potentially resulting in financial penalties or delays in processing. Recognizing and avoiding these errors is crucial for individuals and businesses alike.

To ensure a smooth and compliant submission process, individuals and businesses should carefully review each section of the Connecticut OP-300 form, adhere strictly to the instructions provided, and double-check their calculations and attached schedules. Taking these steps can help avoid common pitfalls and ensure that the process is completed efficiently and accurately.

Moreover, consulting with a professional or contacting the Excise Taxes Unit directly for clarification on complex issues can be invaluable. Utilizing resources like the DRS website for additional forms, publications, and guidance could also provide much-needed support during the tax return preparation process.

When managing tobacco taxes in Connecticut, the Department of Revenue Services Form OP-300, also known as the Tobacco Products Tax Return, is a critical document. However, to accurately report and comply with state tax regulations, several other forms and documents may also be necessary. Understanding these additional forms can streamline the tax filing process, ensuring compliance and accuracy in reporting.

In sum, the comprehensive reporting of tobacco products taxes in Connecticut requires careful attention to the main form, OP-300, and an understanding of how each of these additional schedules and forms interplay with it. Effective reporting not only involves filling out the OP-300 with accuracy but also knowing which schedules are pertinent to your specific circumstance, ensuring all tobacco product transactions are correctly accounted for and conform to Connecticut state tax regulations.

The Connecticut OP-300 form, which is used for reporting and paying taxes on tobacco products within the state, shares similarities with other tax forms in various jurisdictions that also focus on the taxation of specific goods. Here are a couple of examples:

The New York State Cigarette and Tobacco Products Tax Return: Similar to the Connecticut OP-300 form, New York's equivalent requires distributors to report the amount of tobacco products, beyond just cigarettes, that were purchased, imported, or manufactured within the state for tax purposes. Both forms calculate taxes based on quantities of products, such as the total number of cigars or total weight of tobacco, and apply specific tax rates to these amounts to determine the total tax due. Additionally, they require detailed information about the business filing the return, including the tax registration number and federal employer identification number (FEIN), ensuring that the state can efficiently track and collect taxes from companies distributing tobacco products within their jurisdictions.

The California Cigarette & Tobacco Products Excise Tax Return: This form closely mirrors the Connecticut OP-300 in its purpose to collect state taxes on the distribution of tobacco products. Both the California and Connecticut forms necessitate the disclosure of detailed transactions covering the sale, importation, manufacturing, and exporting of tobacco products within a specified reporting period. They also require information about untaxed purchases and calculate penalties and interest for late payments. The emphasis on comprehensive details like the product type (e.g., cigars, snuff) and related quantities ensures accurate tax assessment and compliance with state laws governing tobacco sales and distribution.

When completing the Connecticut OP-300 form, a tax return for tobacco products, it's essential to follow specific guidelines to ensure accuracy and compliance with state tax laws. Here are seven dos and don'ts to guide you through the process:

Do:When it comes to navigating the intricacies of state tax forms, misunderstandings can easily arise. This is particularly true for the Connecticut Op 300 Form, a crucial document for those dealing with tobacco products in the state. Let’s demystify some common misconceptions surrounding this form.

The form is only for businesses selling tobacco products to consumers. In reality, the Connecticut Op 300 Form must be filled out by anyone who purchases, imports, receives, acquires, manufactures, or distributes tobacco products within the state, not just those selling directly to end consumers.

It's not necessary to file if no tax is due. Regardless of whether tax is due, taxpayers must file a return for each calendar month by the twenty-fifth day of the following month. This means even if you owe nothing, you still have to submit the form.

Only tobacco products bought or sold in Connecticut need to be reported. The form requires reporting on all tobacco products handled by the entity, including those that are exported out of Connecticut or sold to the federal government.

Snuff is treated the same as other tobacco products for tax purposes. Snuff tobacco products are actually taxed differently, with specific lines on the form (Lines 9 to 12) dedicated to calculating the tax due based on total ounces, rather than the 50% value used for other tobacco products.

Cigars priced at $1.00 or below are subject to tax. The form distinguishes between cigars based on their price, with a specific exemption for cigars in excess of $1.00 per cigar under certain calculations. This highlights the importance of accurately reporting the price and quantity of cigars handled.

You can only pay the tax due with a check. While you can pay by check, the Department of Revenue Services (DRS) also offers an electronic payment option through the Taxpayer Service Center (TSC), providing convenience and flexibility in payment methods.

Personal use of tobacco products doesn't need to be reported. The form does not make exceptions for tobacco products for personal use. If the products meet the criteria for reporting (imported, received, etc., within Connecticut), they must be included in the return.

A preparer’s signature is not necessary. If the return is prepared by someone other than the taxpayer, the preparer’s signature is required. This ensures accountability and verifies the accuracy of the information provided.

Understanding these facets of the Connecticut Op 300 Form is essential for correctly reporting tobacco products and ensuring compliance with state tax regulations. By clearing up these misconceptions, businesses and individuals can better navigate their obligations and avoid potential pitfalls.

Understanding the Connecticut OP-300 form is imperative for tobacco product distributors within the state. Designed to calculate and report the taxes due on tobacco products, excluding certain snuff tobacco products and cigars over $1.00, its precise completion ensures compliance with state tax laws. Here are seven key takeaways for correctly filling out and utilizing this form:

Tackling the Connecticut OP-300 form with diligence and precise attention to detail not only fulfills a legal obligation but also ensures that distributors can confidently navigate the complexities of tobacco product taxation, avoiding penalties and fostering a compliant business environment. For further assistance or clarification on specifics, reaching out to the Excise Taxes Unit or leveraging resources on the Department of Revenue Services website is highly recommended.

Ct Dmv Gift Form - Simplifies the reporting process for stolen vehicles, providing clear instructions and required fields for owners to fill out.

Ct Foi Commission - An indispensable component for UConn alumni and students to mobilize their academic qualifications for various application processes.

Connecticut Fpd 124 - Includes detailed recording features for seller and item information, enhancing traceability and security.