Free Promissory Note Template for Connecticut

Free Promissory Note Template for Connecticut

In the state of Connecticut, individuals seeking to formalize a loan transaction between a lender and a borrower may use a Connecticut Promissory Note form. This essential financial document serves as a legally binding agreement, outlining the terms of the loan, including the principal amount, interest rate, repayment schedule, and any collateral involved. It provides a structured and secure framework for both parties, ensuring clarity and understanding regarding the obligations of the borrower to repay the borrowed funds. Additionally, the form may specify the consequences of default, offering protection to the lender while also providing the borrower with a clear understanding of their financial responsibilities. Given its importance in the lending process, the Connecticut Promissory Note form plays a pivotal role in private financing, empowering lenders and borrowers to engage in transactions with confidence and legal backing.

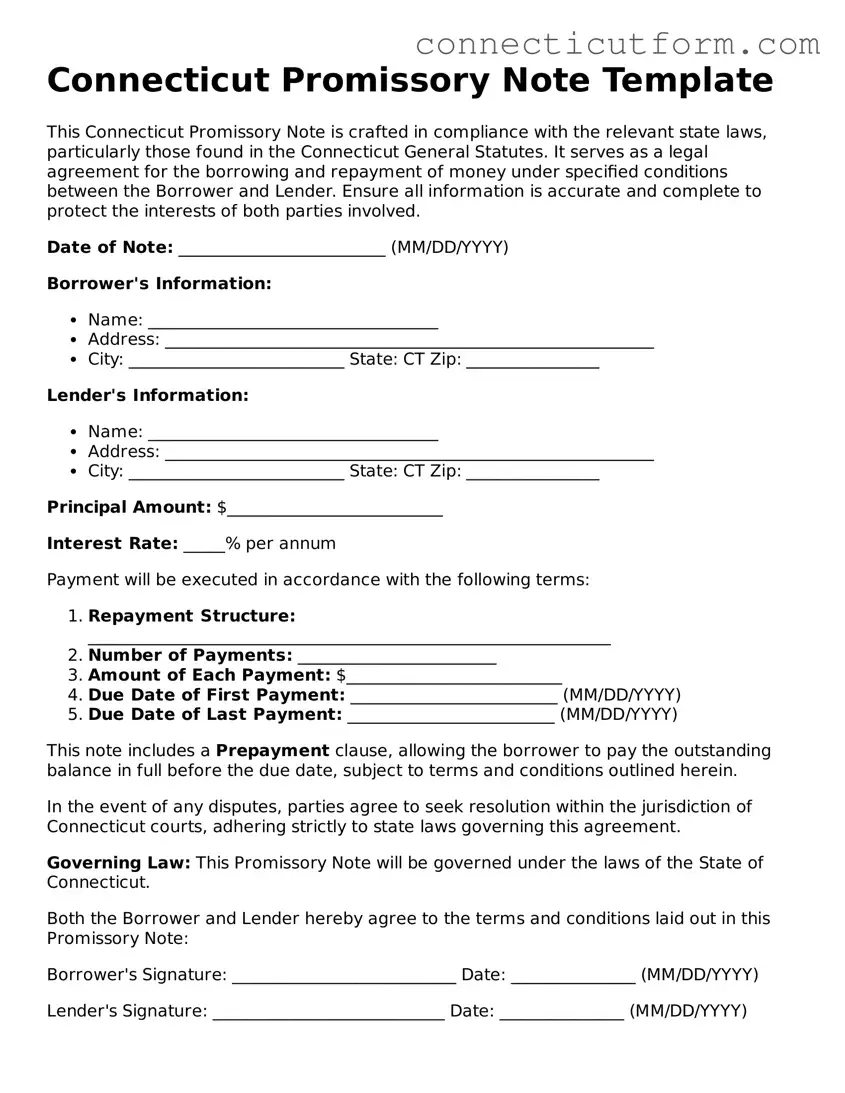

Connecticut Promissory Note Template

This Connecticut Promissory Note is crafted in compliance with the relevant state laws, particularly those found in the Connecticut General Statutes. It serves as a legal agreement for the borrowing and repayment of money under specified conditions between the Borrower and Lender. Ensure all information is accurate and complete to protect the interests of both parties involved.

Date of Note: _________________________ (MM/DD/YYYY)

Borrower's Information:

Lender's Information:

Principal Amount: $__________________________

Interest Rate: _____% per annum

Payment will be executed in accordance with the following terms:

This note includes a Prepayment clause, allowing the borrower to pay the outstanding balance in full before the due date, subject to terms and conditions outlined herein.

In the event of any disputes, parties agree to seek resolution within the jurisdiction of Connecticut courts, adhering strictly to state laws governing this agreement.

Governing Law: This Promissory Note will be governed under the laws of the State of Connecticut.

Both the Borrower and Lender hereby agree to the terms and conditions laid out in this Promissory Note:

Borrower's Signature: ___________________________ Date: _______________ (MM/DD/YYYY)

Lender's Signature: ____________________________ Date: _______________ (MM/DD/YYYY)

Witness's Signature (if applicable): ___________________________ Date: _______________ (MM/DD/YYYY)

| Fact Number | Detail |

|---|---|

| 1 | Connecticut promissory notes are legal agreements used to document a loan between two parties. |

| 2 | They must include the amount of money being loaned and the interest rate. |

| 3 | The repayment schedule, including dates and amounts, needs to be clearly stated in the note. |

| 4 | Interest rates on promissory notes in Connecticut cannot exceed the legal limit set by state law. |

| 5 | If signed, these notes become binding contracts enforceable under Connecticut law. |

| 6 | Secured and unsecured are the two main types of promissory notes. |

| 7 | A secured note is backed by collateral, whereas an unsecured note is not. |

| 8 | Connecticut General Statutes Annotated (CGSA) governs the creation and enforcement of promissory notes. |

| 9 | Failure to comply with the terms of the note can lead to legal action, including collection efforts and lawsuits. |

Filling out a Connecticut Promissory Note form is essential for both lenders and borrowers as it legally documents the loan's details, providing security and clarity for the financial agreement. This document outlines the loan's amount, interest rate, repayment schedule, and any other terms agreed upon by the parties. Below is a concise, easy-to-follow guide for completing the form accurately to ensure all legal requirements are met.

After completing these steps, make sure both the lender and borrower retain copies of the promissory note for their records. This document serves as a crucial legal agreement and can be essential for resolving any disputes that might arise regarding the loan. Filing the document in a safe place is recommended, ensuring it can be easily accessed when needed.

What is a Connecticut Promissory Note form?

A Connecticut Promissory Note form is a legal document used to outline the details of money borrowed between two parties in the state of Connecticut. This form serves as a written promise that the borrower will repay the lender the amount of money borrowed, along with any agreed-upon interest, over a specified period.

Is a Connecticut Promissory Note form legally binding?

Yes, when properly executed, a Connecticut Promissory Note form is a legally binding agreement between the lender and the borrower. It obligates the borrower to repay the loan as agreed, making it enforceable in a court of law if necessary.

What key elements should be included in a Connecticut Promissory Note?

A comprehensive Connecticut Promissory Note should include:

Do I need a witness or notary for a Connecticut Promissory Note?

While not always required, having a witness or notarizing the promissory note can add an extra layer of legal protection and authenticity to the document. It can help confirm that the signatures are genuine, especially if the agreement is disputed in the future.

Can interest be charged on a Connecticut Promissory Note, and is there a maximum rate?

Interest can be charged on a Connecticut Promissory Note. However, the state has usury laws that cap the maximum interest rate that can be charged. The legal maximum rate can vary, so it is recommended to check the current statutes to ensure compliance.

What happens if the borrower does not repay according to the Connecticut Promissory Note terms?

If the borrower fails to repay the loan as agreed, the lender may take legal action to enforce the repayment of the debt. This could include suing for the outstanding balance or taking possession of any collateral that was used to secure the loan.

Is a promissory note the same as a loan agreement?

While similar, a promissory note and a loan agreement are not the same. A promissory note is a simpler document that includes the promise to pay back the money borrowed. A loan agreement is more detailed, outlining the responsibilities and obligations of both parties in addition to the repayment terms.

Can a Connecticut Promissory Note be modified?

Yes, a Connecticut Promissory Note can be modified if both the lender and borrower agree to the changes. Any modifications should be made in writing, and both parties should sign the amended document to ensure the changes are legally binding.

Where can I find a Connecticut Promissory Note form?

Connecticut Promissory Note forms can be found online through legal resources or by consulting with a legal professional who can provide a form that meets your specific needs and complies with Connecticut state law.

When individuals set out to complete the Connecticut Promissary Note form, their objective is to ensure a smooth lending process. However, a few common mistakes can complicate things, leading to potential misunderstandings or legal issues down the line. By being aware of these pitfalls, parties can better protect their interests and foster a positive lending relationship.

One primary mistake is not stating the full legal names of the involved parties. This detail might seem minor but is crucial for the clarity and enforceability of the note. Using nicknames or shortened versions of names can lead to confusion about the parties' identities, especially in legal contexts.

Another issue is inaccurately defining the terms of repayment. The Connecticut Promissory Note form requires specific details about repayment schedules, including dates, amounts, and intervals. Sometimes, individuals might leave these sections incomplete or vague, which can lead to disagreements about what was mutually agreed upon. It's crucial that this information is laid out clearly to prevent any misunderstandings.

Failure to specify the interest rate is also a common stumbling block. In Connecticut, there are legal limits to the amount of interest that can be charged on a personal loan. If the promissory note does not clearly state the interest rate, or if the rate is above the legal limit, this could render the whole agreement void or unenforceable.

Forgetting to include a clause about late fees or missed payment penalties is another oversight. While nobody likes to think about the possibility of missed payments, having a predetermined course of action outlined in the note helps manage expectations and protects both the lender and the borrower.

Last but not least, not having the document witnessed or notarized can undermine its legitimacy. While not always legally required, having an impartial third party witness the signing can add an extra layer of verification and can be crucial in cases where the validity of the signatures is questioned.

In summary, when filling out the Connecticut Promissory Note form, individuals should ensure they:

By avoiding these common mistakes, lenders and borrowers can create a promissory note that is clear, fair, and enforceable. This careful attention to detail can help prevent disputes and foster a more trustworthy and reliable lending process.

When you're dealing with a Connecticut Promissory Note, you are likely engaging in a financial transaction that necessitates clarity and legality. Such transactions do not exist in a vacuum, often being part of a larger financial, legal, or personal relationship between parties. As such, there may be several additional documents that are used alongside a Connecticut Promissory Note to ensure that all aspects of the transaction are properly addressed and legally sound. Here is a look at some of these important accompanying documents.

Each of these documents plays a crucial role in ensuring the security and legality of financial transactions involving a Connecticut Promissory Note. Whether you're lending or borrowing, understanding and properly using these documents can help to protect your interests and facilitate a smoother transaction. It is often wise to consult with a legal professional to ensure that all documents are correctly executed and legally binding.

The Connecticut Promissory Note form is similar to a personal loan agreement, in that both set out the terms under which money is being lent and must be repaid. A key difference, however, is that the promissory note is usually simpler and more straightforward. It outlines the amount borrowed, the interest rate, if any, the repayment schedule, and the consequences of non-payment. Personal loan agreements, while similar in content, tend to be more detailed and include additional clauses such as representations and warranties, covenants, and conditions precedent to the loan.

Another document akin to the Connecticut Promissory Note form is an IOU (I Owe You). Both serve as written promises of debt repayment. However, an IOU is less formal and typically does not include detailed terms of repayment such as payment schedules, interest rates, or security agreements. An IOU simply acknowledges that a debt exists, whereas a promissory note explains how that debt will be repaid, making the promissory note a more comprehensive document.

The form is also comparable to a mortgage agreement, in the context that both involve a borrower promising to repay a sum of money. The critical difference is that a mortgage agreement is secured by the borrower’s property, which the lender can take ownership of if the borrower fails to repay the loan. While a promissory note can also be secured or unsecured, its focus is primarily on the repayment of the loan itself rather than detailing the security interest in the property.

When filling out the Connecticut Promissory Note form, it is crucial to approach the task with diligence and accuracy to ensure that all parties understand their obligations and rights. To aid in this process, here are essential dos and don'ts to keep in mind:

Do:

Don't:

When it comes to understanding the specifics of promissory notes in Connecticut, there are several misconceptions that can lead to confusion. Here are five common ones:

A belief exists that any form of a promissory note will suffice in Connecticut. However, for a promissory note to be legally binding in the state, it must meet specific requirements, such as clear terms of repayment, interest rates, and the signatures of both the lender and borrower.

Many people think that promissory notes do not need to be witnessed or notarized in Connecticut. While not every state requires this, having these precautions in place can provide legal strength to the document, especially if there is a dispute.

There's a misconception that promissory notes are only for personal loans between individuals. In reality, they can be utilized in a wide range of lending situations, including business loans and real estate transactions.

Some believe that the interest rate on a Connecticut promissory note can be as high as the parties agree upon. This is untrue; the state imposes a maximum interest rate to prevent usury. Agreements violating these regulations are not enforceable.

It is also wrongly assumed that in Connecticut, if the borrower does not repay the loan, the lender has few legal options to recover the debt. The law provides various mechanisms for debt enforcement, including but not limited to, filing a lawsuit to obtain a judgment against the borrower.

Understanding these common misconceptions can help parties involved in the creation of a promissory note in Connecticut to ensure that their document is legal, comprehensive, and enforceable.

When considering the use of a Connecticut Promissory Note form, it is essential to carefully navigate its completion and application to ensure that its execution accurately represents the agreement between the parties involved. Here are seven key takeaways about filling out and using this form effectively:

Ct Temporary Plates - Including a section for seller disclosures about the ATV's condition and history can provide peace of mind and transparency for the buyer.

Can I Register a Trailer Online in Ct - This form ensures that all relevant taxes on the transaction are duly noted, potentially including sales tax or use tax, based on the boat’s sale price.

Release and Hold Harmless Agreement - It provides a legal framework for indemnity, ensuring one party can compensate another without the threat of a lawsuit.